Archive for December, 2013

Top Posts of 2013

| Peter Klein |

It’s been another fine year at O&M. 2013 witnessed 129 new posts, 197,531 page views, and 114,921 unique visitors. Here are the most popular posts published in 2013. Read them again for entertainment and enlightenment!

- Rise of the Three-Essays Dissertation

- Ronald Coase (1910-2013)

- Sequestration and the Death of Mainstream Journalism

- Post AoM: Are Management Types Too Spoiled?

- Nobel Miscellany

- The Myth of the Flattening Hierarchy

- Climate Science and the Scientific Method

- Bulletin: Brian Arthur Has Just Invented Austrian Economics

- Solution to the Economic Crisis? More Keynes and Marx

- Armen Alchian (1914-2013)

- My Response to Shane (2012)

- Your Favorite Books, in One Sentence

- Does Boeing Have an Outsourcing Problem?

- Doug Allen on Alchian

- New Paper on Austrian Capital Theory

- Hard and Soft Obscurantism

- Mokyr on Cultural Entrepreneurship

- Microfoundations Conference in Copenhagen, June 13-15, 2014

- On Academic Writing

- Steven Klepper

- Entrepreneurship and Knowledge

- Easy Money and Asset Bubbles

- Blind Review Blindly Reviewing Itself

- Reflections on the Explanation of Heterogeneous Firm Capability

- Do Markets “React” to Economic News?

Thanks to all of you for your patronage, commentary, and support!

Pirrong Responds

| Peter Klein |

Here’s Craig’s initial (and hopefully not final!) response to David Kocieniewski’s “farrago of dishonesty, insinuations, innuendo, and ad hominem.” As expected, Craig pulls no punches. Kocieniewski’s failure to point out that most of Craig’s professional work argues against the interests of his alleged paymasters “betrays his utter unprofessionalism and bias, and is particularly emblematic of the shockingly shoddy excuse for journalism that his piece represents.” The insinuation that Craig’s paid work deals with speculation, when none of it does, is “misleading, deceptive, and plainly libelous.” The Times piece is riddled with factual and chronological errors, deliberately inserted to score political points: “dishonest to its very core because of its egregiously biased omission of some essential material facts and deceptive presentation of others.” I can’t say I’m surprised; this is mainstream journalism, after all.

Craig also provides this roundup of posts defending him and Scott Irwin, including ours.

NYT Smears Craig Pirrong, Scott Irwin

| Peter Klein |

The NYT runs a hatchet-job on the brilliant financial economist (and former O&M guest blogger) Craig Pirrong. Apparently Craig not only does academic research on commodity markets and participates in public policy debates about commodity-market regulation but also — gasp! — is a paid consultant for commodity-trading firms. Without detailing any specific impropriety, the Times implies that Craig is little more than a shill for big evil corporations, or something. “Academics Who Defend Wall St. Reap Reward,” screams the Times headline.

Thousands of economists are paid consultants for the Federal Reserve System, World Bank, IMF, USDA, and virtually every government agency around the world, but you will never hear the Times suggest that their research or public advocacy could in the slightest way be compromised by these ties. As Larry White and E. C. Pasour have pointed out, the academic work funded by government agencies nearly always — surprise! — comes out in defense of those agencies, their missions, and their generous contributions to the public good. Did the prospect of heading the world’s most powerful economic planing agency influence Janet Yellen’s public testimony, her research, or her leadership at the San Francisco Fed? Can you imagine a Times headline, “Academics Who Defend Fed Reap Reward”?

Scott Irwin, a distinguished agricultural economist at the University of Illinois is also targeted. Again, the message is clear. If you oppose the Times’s editorial position on regulation (or any other issue), you are compromised by financial or other ties. If you support the Times’s position, you are a scholar or public figure of great integrity.

Update: See also Felix Salmon’s excellent summary of the “non-scandal.”

Walter Oi, 1929-2013

| Nicolai Foss |

Walter Oi died December 24. Oi was famous for two things, namely for being a highly active academic in spite of being totally blind (after 1956), and for estimating the social costs of the draft (here). However, he contributed to many areas of applied price theory in a highly original fashion. Of possibly particular interest to strategic management scholars is his 1983 paper on how heterogeneous “entrepreneurial ability” and differential monitoring constrains the size, product offerings and organization of firms in equilibrium. Here is Steve Landsburg’s long, detailed and moving obituary for Oi.

Rate My Journals

| Peter Klein |

Researchers: You rate products and sellers on Amazon and Ebay, you describe your travel experiences on TripAdvisor, and your students judge you on ratemyprofessors.com. I don’t know any systematic evidence on this, but consultants and journalists seem to think that companies are better off letting customers rate (and rant) online, even if this makes it more difficult to manage the brand.

A new venture called SciRev is encouraging researchers to rate their experiences with particular journals: how long are papers turned around, how good are the referee reports, how responsive is the editorial office. It’s not quite open-source peer review, because the specific papers and authors are anonymous (as far as I can tell), but it represents an interesting experiment in opening up the publishing process, at least in terms of author feedback on journals.

SciRev is a website made by researchers for researchers. The information provided by you and your fellow authors is freely available to the entire research community. In this way we aim to make the scientific review process more transparent. Efficient journals get credits for their efforts to improve their review process and the way they handle manuscripts. Less efficient journals are stimulated to put energy in organizing things better. Researchers can search for a journal with a speedy review procedure and have their papers published earlier. Editors get the opportunity to compare their journal’s performance with that of others and to provide information about their journal at our website.

SciRev aims to help science by making the peer review process more efficient. This process is one of the weakest links in the process of scientific knowledge production. Valuable papers may spent several months to over a year at reviewers’ desks and editorial offices before a decision is taken. This is a serious time loss in a process that in other respects has become much more efficient in the last decades. SciRev helps speeding up this process by making it more transparent. Researchers get the possibility to share their review experiences with their colleagues, who therefore can make a better informed choice for a journal to submit their work to. Journals that manage to set up a more efficient review process and which handle manuscripts better are rewarded for this and may attract more and better manuscripts.

There are only a few reviews at this point, so not much information to consume, but I like the concept. And I may be submitting some reviews of my own… (Thanks to Bronwyn Hall for the tip.)

Business Groups in the US

| Peter Klein |

Diversification continues to be a central issue for strategic management, industrial organization, and corporate finance. There are huge research and practitioner literatures on why firms diversify, how diversification affects financial, operating, and innovative performance, what underlies inter-industry relatedness, how diversification ties into other aspects of firm strategy and organization, whether diversification is driven by regulation or other policy choices, and so on. There are many surveys of these literatures (Lasse and I contributed this one).

Some of the most interesting research deals with the institutional environment. For example, many US corporations were widely diversified in the 1960s and 1970s when the brokerage industry was small and protected by tough legal restrictions on entry, antitrust policy frowned on vertical and horizontal growth (maybe), and a volatile macroeconomic environment encouraged internalization of inter-firm transactions (also maybe). After the brokerage industry was deregulated in 1975, the antitrust environment became more relaxed, and the market for corporate control heated up, many conglomerates were restructured into more efficient, specialized firms. To quote myself:

The investment community in the 1960s has been described as a small, close-knit group wherein competition was minimal and peer influence strong (Bernstein, 1992). As Bhide (1990, p. 76) puts it, “internal capital markets … may well have possessed a significant edge because the external markets were not highly developed. In those days, one’s success on Wall Street reportedly depended far more on personal connections than analytical prowess.” When capital markets became more competitive in the 1970s, the relative importance of internal capital markets fell. “This competitive process has resulted in a significant increase in the ability of our external capital markets to monitor corporate performance and allocate resources” (Bhide, 1990, p. 77). As the cost of external finance has fallen, firms have tended to rely less on internal finance, and thus the value added from internal-capital-market allocation has fallen. . . .

Similarly, corporate refocusing can be explained as a consequence of the rise of takeover by tender offer rather than proxy contest, the emergence of new financial techniques and instruments like leveraged buyouts and high-yield bonds, and the appearance of takeover and breakup specialists like Kohlberg Kravis Roberts, which themselves performed many functions of the conglomerate headquarters (Williamson, 1992). A related literature looks at the relative importance of internal capital markets in developing economies, where external capital markets are limited (Khanna and Palepu 1999, 2000).

The key reference is to Amar Bhide’s 1990 article “Reversing Corporate Diversification,” which deserves to be better known. But note also the pointer to Khanna and Palepu’s important work on diversified business groups in emerging markets, which has also led to a vibrant empirical literature. The idea there is that weak institutions lead to poorly performing capital and labor markets, leading firms to internalize functions that would otherwise be performed between firms. More generally, firm strategy and organization varies systematically with the institutional environment, both over time and across countries and regions.

Surprisingly, diversified business groups were also common in the US, in the early 20th century, which brings me (finally) to the point of this post. A new NBER paper by Eugene Kandel, Konstantin Kosenko, Randall Morck, and Yishay Yafeh studies these groups and reaches some interesting and provocative conclusions. Check it out:

Eugene Kandel, Konstantin Kosenko, Randall Morck, Yishay Yafeh

NBER Working Paper No. 19691, December 2013The extent to which business groups ever existed in the United States and, if they did exist, the reasons for their disappearance are poorly understood. In this paper we use hitherto unexplored historical sources to construct a comprehensive data set to address this issue. We find that (1) business groups, often organized as pyramids, existed at least as early as the turn of the twentieth century and became a common corporate form in the 1930s and 1940s, mostly in public utilities (e.g., electricity, gas and transportation) but also in manufacturing; (2) In contrast with modern business groups in emerging markets that are typically diversified and tightly controlled, many US groups were focused in a single sector and controlled by apex firms with dispersed ownership; (3) The disappearance of US business groups was largely complete only in 1950, about 15 years after the major anti-group policy measures of the mid-1930s; (4) Chronologically, the demise of business groups preceded the emergence of conglomerates in the United States by about two decades and the sharp increase in stock market valuation by about a decade, so that a causal link between these events is hard to establish, although there may well be a connection between them. We conclude that the prevalence of business groups is not inconsistent with high levels of investor protection; that US corporate ownership as we know it today evolved gradually over several decades; and that policy makers should not expect policies that restrict business groups to have an immediate effect on corporate ownership.

Postrel on Dynamic Capabilities

| Peter Klein |

Former guest blogger Steve Postrel weighs in on the future of the dynamic capabilities approach (reprinted, with permission, from a thread on Academia.edu). Steve responds to the question, “Is the dynamic capabilities approach outdated?” with some typical insightful remarks.

Since DC is primarily an ex post facto construct measured by sampling on the dependent variable — i.e., if the firm successfully adapts, then it had DC — its prominence is not a sign that it is doing much intellectual work. . . .

[T]o a first approximation, arguments for the importance of DC have tended to be of the form “We know a priori that firms need to be able to change their operational capabilities from time to time; we have examples of successful firms that have adapted in this way and examples of less-successful firms that haven’t; therefore we can say that the successful adapters had more of this valuable thing we will call ‘dynamic capability.'”

Certainly there have been empirical papers that do better than that, by, for example, trying to look at firms that have adapted multiple times, or by identifying specific organizational structures and practices that might enhance adaptability. The difficult issue with looking at a “precursor” like experience is that theoretically experience could reduce DC by causing specialization and lock-in. Other putative precursors suffer from the ex post measurement problem — how do we know if a firm has the right knowledge for adaptation until we see whether it succeeds?

I suspect there are also deeper conceptual problems because DC is equivocal even with perfect measurement. It would be pretty hard to specify what one meant by the “amount” of DC a firm has or to compare the “amounts” that any two firms have. DC is certainly not a completely ordering relation and I’m not sure it’s even a partial order. Without presenting formal models and going back and forth between those and peoples’ intuition about what DC is “supposed” to mean, however, one really can’t pin these problems down enough to tell if they are serious. . . . (more…)

Kirzner and Entrepreneurship Research

| Peter Klein |

Per Bylund and I have written a paper on Israel Kirzner’s influence on the entrepreneurship literature. It’s titled “The Place of Austrian Economics in Contemporary Entrepreneurship Research” but deals mainly with Kirzner. Comments are appreciated.

Per Bylund and I have written a paper on Israel Kirzner’s influence on the entrepreneurship literature. It’s titled “The Place of Austrian Economics in Contemporary Entrepreneurship Research” but deals mainly with Kirzner. Comments are appreciated.

The paper was written for a forthcoming special issue of the Review of Austrian Economics on Kirzner’s contributions. We take a nuanced position: While Kirzner’s work underlies the dominant opportunity-discovery perspective in the entrepreneurship research literature, this perspective is increasingly challenged among entrepreneurship scholars, for some of the same reasons that Kirzner’s theoretical framework has been criticized by his fellow Austrian economists. Nonetheless, it is impossible to make progress in entrepreneurship studies, or the Austrian analysis of the market, without engaging Kirzner’s ideas.

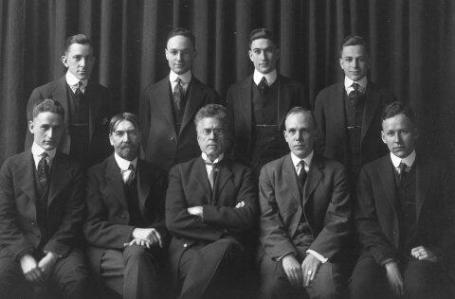

Veblen and Davenport

| Peter Klein |

Further to my earlier post on Veblen at Missouri, here’s a newly discovered photo of the university’s Faculty of Commerce from the mid nineteen-teens, featuring Dean Herbert J. Davenport in the center with Veblen to his right. (Thanks to @MizzouBusiness for the find.)

Entrepreneurship, Financial Capital, and Social Capital

| Peter Klein |

Two interesting new papers on entrepreneurship. The first deals with financial capital — specifically, the degree to which entrepreneurship (defined as self-employment) is constrained by credit availability. As regular readers know, I’ve been crusading against the idea that entrepreneurship consists of recognizing opportunities, in favor of the alternative idea that entrepreneurship involves putting assets at risk. The latter view directs our attention to how entrepreneurial activities are funded; rather than assuming that all positive-NPV opportunities are exploited, we should focus on the investor’s decision to allocate risk capital to one or another potential project. Put simply, “entrepreneurship is exercised not only by founders, but by funders.”

Funders care about collateral, which suggests that self-employment is constrained by the availability of durable personal assets like housing. In a new NBER working paper, “Housing Collateral and Entrepreneurship,” Martin Schmalz, David Sraer, and David Thesmar find a strong correlation between self-employment and house prices. “Our empirical strategy uses variations in local house prices as shocks to the value of collateral available to individuals owning a house and controls for local demand shocks by comparing entrepreneurial activity of homeowners and renters operating in the same region. We find that an increase in collateral value leads to a higher probability of becoming an entrepreneur. Conditional on entry, entrepreneurs with access to more valuable collateral create larger firms and more value added, and are more likely to survive, even in the long run.”

My Missouri colleague Colleen Heflin, along with Seok-Woo Kwon and Martin Ruef, have a new paper in the American Sociological Review on social capital and self-employment. Many papers have examined how an individual’s “social capital” — defined as networks of social and professional relationships — affects various economic outcomes, including the propensity to start a firm. Colleen and her colleagues focus at the community level and find that “individuals in communities with high levels of social trust are more likely to be self-employed compared to individuals in communities with lower levels of social trust. Additionally, membership in organizations connected to the larger community is associated with higher levels of self-employment, but membership in isolated organizations that lack connections to the larger community is associated with lower levels of self-employment.”

Of course, self-employment is only a crude proxy for entrepreneurship in the functional sense, but it is a widely used proxy in the empirical literature. I suppose entrepreneurship researchers, like other social scientists, resemble the drunk looking for his car keys under the lamppost. Who am I to complain?

ISNIE 2014

| Peter Klein |

![]() The ISNIE 2014 Call for Papers is now available. The conference is at Duke University, 19-21 June 2014, home of President-Elect and Program Committee Chair John de Figueiredo. Bob Gibbons and Timur Kuran are keynote speakers. ISNIE is one of our favorite conferences, so please consider submitting a proposal! Submissions are due 30 January 2014.

The ISNIE 2014 Call for Papers is now available. The conference is at Duke University, 19-21 June 2014, home of President-Elect and Program Committee Chair John de Figueiredo. Bob Gibbons and Timur Kuran are keynote speakers. ISNIE is one of our favorite conferences, so please consider submitting a proposal! Submissions are due 30 January 2014.

Your Favorite Books, in One Sentence

| Peter Klein |

Craig Newmark pointed me to this list of “15 Famous Business Books Summarized In One Sentence Each.” I don’t think highly of any of the books on the list except Innovator’s Dilemma, but it’s an interesting exercise. Care to try your hand? I’ll start:

Oliver Williamson, Economic Institutions of Capitalism: Be shrewd in your dealings with suppliers and customers; they may not do what they promised.

Edith Penrose, Theory of the Growth of the Firm: The more you do what you’re good at, the better you get at similar things that may surprise you.

Ludwig von Mises, Bureaucracy: Fixed rules are better than employee discretion when you’re producing stuff that isn’t bought and sold on markets.

Michael Porter, Competitive Strategy: Be efficient and productive, but pay attention to your rivals and partners, or they’ll eat you for lunch.

John Maynard Keynes, The General Theory: Chicken chicken chicken, chicken chicken chicken chicken chicken.

Recent Comments