Author Archive

Clusters of Entrepreneurship and Innovation

| Peter Klein |

That’s the title of a new review paper by Aaron Chatterji, Ed Glaeser, and William Kerr (a gated NBER working paper, unfortunately). Agglomeration has been a huge issue in the entrepreneurship, technology strategy, innovation policy, and economic growth literatures and it’s nice to have an up-to-date, not-very-technical review paper. (Hopefully there is an ungated copy out there somewhere.)

Clusters of Entrepreneurship and Innovation

Aaron Chatterji, Edward L. Glaeser, William R. Kerr

NBER Working Paper No. 19013, May 2013This paper reviews recent academic work on the spatial concentration of entrepreneurship and innovation in the United States. We discuss rationales for the agglomeration of these activities and the economic consequences of clusters. We identify and discuss policies that are being pursued in the United States to encourage local entrepreneurship and innovation. While arguments exist for and against policy support of entrepreneurial clusters, our understanding of what works and how it works is quite limited. The best path forward involves extensive experimentation and careful evaluation.

Update: ungated version here.

Google-Linked Scholarship

| Peter Klein |

Have you noticed that when you search for a person on Google, the sidebar shows you other linked people searches (“People also search for”)? E.g., if you search for yours truly, it pulls up Nicolai Foss, Joe Salerno, Bob Murphy, and Israel Kirzner. I’m not sure how the algorithm works; is it the likelihood these searches are combined, or searched in sequence, or does it have to do with cross-links in search results? Anyway, it’s interesting to see who Google things is related to whom. For instance

Peter G. Klein ==> Nicolai Foss, Joseph Salerno, Robert P. Murphy, Israel Kirzner

Nicolai Foss ==> Peter G. Klein, Edith Penrose, Israel Kirzner, Oliver E. Williamson

Oliver E. Williamson ==> Ronald Coase, Elinor Ostrom, Douglass North, Armen Alchian

Murray N. Rothbard ==> Ludwig von Mises, Friedrich Hayek, Frédéric Bastiat, Henry Hazlitt

Paul Krugman ==> John Law, P. T. Barnum, Charles Ponzi, Beelzebub

The Klein Revolution

| Peter Klein |

Going through some old files, I came across a 1995 Wall Street Journal piece I had saved, with the following passages highlighted:

Mr. Klein caught the fanaticism of the converted and convened a special commission to audit the books. It summed up its findings in six words: the need for change is urgent. Polls showed the public agreed. . . .

Mr. Klein doggedly pursued a program of breathtaking change. Government will fall from 24,000 to 18,000 in two and a half years. Sixty school boards were eliminated, the health budget was cut by 17%, and the number of hospital beds cut in half. Seniors earning over $21,000 (U.S.) a year were asked to pay their own Medicare premiums. . . .

The Klein Revolution did meet with opposition. . . . “My day wasn’t complete without a protest,” Mr. Klein recalls with a smile. But each success spurred him on: “You’re nervous the first time you try something new, but once you do it, you sort of get used to it.” . . .

Last year, he spoke to a group in Toronto and was asked if books by F.A. Hayek and Ludwig von Mises had inspired his policies. Mr. Klein smiled and said, . . . “Do I look like the kind of guy who would read those books?” The crowd laughed, because while Mr. Klein may not have read Hayek’s “The Road to Serfdom,” he has proved he knows how to build a policy exit ramp away from it.

The full article is below the fold. (more…)

Hart on Incomplete Contracts

| Peter Klein |

Transaction cost economics, the property-rights approach to the firm, and the judgment-based view all assume that contracting parties cannot sign complete, contingent contracts, in which case firm boundaries would be arbitrary and unimportant. TCE tends to attribute incompleteness to bounded rationality, while the judgment-based view appeals to Knightian uncertainty and subjectivism to describe markets for judgment are incomplete. The property-rights approach of Grossman, Hart, and Moore did not have an explicit theory of incompleteness, which critics such as Maskin and Tirole saw as a major weakness.

Oliver Hart has written a series of recent papers on “reference points” as a new explanation for incompleteness. The newest, released today as an NBER working paper (with Maija Halonen-Akatwijuka), is the most explicit. It argues that parties deliberately leave gaps in contracts because explicit clauses can make it more difficult for parties to parties to renegotiate after the fact. Check it out and see what you think.

More is Less: Why Parties May Deliberately Write Incomplete Contracts

Maija Halonen-Akatwijuka, Oliver D. Hart

NBER Working Paper No. 19001, April 2013Why are contracts incomplete? Transaction costs and bounded rationality cannot be a total explanation since states of the world are often describable, foreseeable, and yet are not mentioned in a contract. Asymmetric information theories also have limitations. We offer an explanation based on “contracts as reference points”. Including a contingency of the form, “The buyer will require a good in event E”, has a benefit and a cost. The benefit is that if E occurs there is less to argue about; the cost is that the additional reference point provided by the outcome in E can hinder (re)negotiation in states outside E. We show that if parties agree about a reasonable division of surplus, an incomplete contract can be strictly superior to a contingent contract.

Shelanski Tapped for Top Regulatory Post

| Peter Klein |

My old classmate, fellow Oliver Williamson student, and coauthor Howard Shelanski has been nominated to head the Office of Information and Regulatory Affairs (the post typically described as Regulation Czar). Howard was in the joint PhD-JD program at Berkeley, went on to clerk for Antonin Scalia, joined the faculty at Berkeley’s School of Law, and served in a number of regulatory posts before moving to Georgetown. He currently heads the FTC’s Bureau of Economics.

My old classmate, fellow Oliver Williamson student, and coauthor Howard Shelanski has been nominated to head the Office of Information and Regulatory Affairs (the post typically described as Regulation Czar). Howard was in the joint PhD-JD program at Berkeley, went on to clerk for Antonin Scalia, joined the faculty at Berkeley’s School of Law, and served in a number of regulatory posts before moving to Georgetown. He currently heads the FTC’s Bureau of Economics.

Howard’s a super-smart guy, whom I’d describe as an antitrust moderate (unlike me, an anti-antitrust extremist). He’s sympathetic to “post Chicago” antitrust theory and policy, but more of a nuts-and-bolts, case-by-case guy. I’m not a fan Cass Sunstein, current head of the OIRA, and I expect to like Howard’s performance much better. Howard doesn’t share Sunstein’s enthusiasm for behavioral analysis, for example, as seen in an interview last December, where he said this about the role of behavioral economics in antitrust:

I think there is a role, but one needs to be very modest and cautious. There has been a lot written and a lot said about how behavioral economics fundamentally undermines the models on which we do antitrust analysis. And I think most people involved with antitrust enforcement, most people who think about competition issues, would disagree that there is some fundamental new paradigm shift in the works. But behavioral economics does supply insights into how consumers might respond to certain kinds of information, contracting practices, or pricing schemes. This can be very useful to understanding certain kinds of market performance and has led to greater modesty about imputing perfect foresight or rationality to consumers.

But one needs to understand that that is not the sign of a broader behavioral economics revolution in antitrust.

My general feelings about regulatory czars are well summarized by this passage from Fiddler on the Roof, quoted today by Danny Sokol in the same context:

Young Jewish Man: Rabbi, may I ask you a question?

Rabbi: Certainly, my son.

Young Jewish Man: Is there a proper blessing for the Tsar?

Rabbi: A blessing for the Tsar? Of course! May God bless and keep the Tsar . . . far away from us!

Critical Agrifood Scholarship

| Peter Klein |

A friend tipped me off to this, um, interesting paper on farmers markets, which the authors place within the larger field of “critical agrifood scholarship.” We all know what “critical” means, and I’m familiar with much of the agrifood literature, but I didn’t know about this particular field. I learned a lot from the paper about the slow-food movement’s ability to “create political transformation,” and build a “radicalized space” even though such markets “cluster around property and privilege.” The authors seek to “unpack the racialized and class-inflected narratives at play in farmers markets [and] to extend the alternative agriculture movement’s strategic rupturing of the veil of commodity fetishism to include the systemic inequalities on which both conventional and alternative agriculture depend.” How about that thesis statement! In passing, the authors manage to chide the slow-food movement’s “complacency with capitalism and consumerism, systems that are inherently exploitative and divisive,” while adding editorial remarks to such important scientific phenomena as “the working class performances of ‘god, guns and country’ that fill the rhetoric of the GOP.”

Thank goodness for taxpayer-subsided universities. If there were a free market for higher education, this kind of valuable scholarship would probably be grossly underfunded.

AMP Symposium on Private Equity

| Peter Klein |

The new issue of the Academy of Management Perspectives features a symposium, edited by Mike Wright, on “Private Equity: Managerial and Policy Implications.” The symposium includes “Private Equity, HRM, and Employment” by Mike with Nick Bacon, Rod Ball, and Miguel Meuleman; “The Evolution and Strategic Positioning of Private Equity Firms” by Robert E. Hoskisson, Wei Shi, Xiwei Yi, and Jing Jin; and “Private Equity and Entrepreneurial Governance: Time for a Balanced View” by John L. Chapman, Mario P. Mondelli, and me. The symposium came out very nicely, if I may say so, covering a variety of strategic, entrepreneurial, and organizational issues related to private equity firms and companies receiving private equity finance.

In his introduction Mike highlights five main contributions:

First, the papers address the need to consider the systematic evidence on the managerial and strategic aspects of PE, in relation to both portfolio firms and PE firms, which has been largely fragmented if not nonexistent. Second, the papers analyze the impact of PE during economic downturns and demonstrate the underlying resilience of PE-backed portfolio firms. Third, the symposium provides an opportunity to develop insights that compare the managerial impact of PE with different forms of ownership and governance. Fourth, the articles in this symposium highlight the heterogeneity of the private equity phenomenon. Finally, in the context of continuing public attention to PE, which has been heightened by the U.S. presidential race and the global recession, the evidence presented in this symposium paints a rather more positive view than the hyperbole of some of the industry’s critics would suggest. Taken together, these contributions indicate a need for caution in attempts to tighten the regulation of PE lest the economic, financial, and social benefits be lost.

The Future of Publishing

| Peter Klein |

![]() The current issue of Nature features a special section on “The Future of Publishing” (thanks to Jason for the tip). The lead editorial discusses the results of a survey of scientists which shows, perhaps surprisingly, that support for online, open-access publishing is lukewarm. It’s not just the commercial publishers who want to maintain the paywalls. The entire issue is filled with interesting stuff, so check it out.

The current issue of Nature features a special section on “The Future of Publishing” (thanks to Jason for the tip). The lead editorial discusses the results of a survey of scientists which shows, perhaps surprisingly, that support for online, open-access publishing is lukewarm. It’s not just the commercial publishers who want to maintain the paywalls. The entire issue is filled with interesting stuff, so check it out.

New Frontiers in Marketing

| Peter Klein |

“Not only do we manufacture here at home, we also economize on bounded rationality while simultaneously safeguarding transactions against the hazards of opportunism!”

Blanchard on Fed Independence

| Peter Klein |

I’ve argued before (1, 2) that the usual arguments for central bank independence aren’t very strong, particularly in the current environment where Bernanke has interpreted the “unusual and exigent circumstances” provision to mean “I will do whatever I want.” (This was a major point in my Congressional testimony about the Fed.) So it was nice to see Olivier Blanchard express similar reservations in an interview published in today’s WSJ (I assume it’s not an April Fool’s Day prank):

One of the major achievements of the last 20 years is that most central banks have become independent of elected governments. Independence was given because the mandate and the tools were very clear. The mandate was primarily inflation, which can be observed over time. The tool was some short-term interest rate that could be used by the central bank to try to achieve the inflation target. In this case, you can give some independence to the institution in charge of this because the objective is perfectly well defined, and everybody can basically observe how well the central bank does..

If you think now of central banks as having a much larger set of responsibilities and a much larger set of tools, then the issue of central bank independence becomes much more difficult. Do you actually want to give the central bank the independence to choose loan-to-value ratios without any supervision from the political process. Isn’t this going to lead to a democratic deficit in a way in which the central bank becomes too powerful? I’m sure there are ways out. Perhaps there could be independence with respect to some dimensions of monetary policy - the traditional ones — and some supervision for the rest or some interaction with a political process.

More on Blogs and Social Media

| Peter Klein |

Nicolai was kind enough to mention my Facebook page but neglected to add that he has one too, and that O&M itself is on Facebook and Twitter. You can read, like, share, and comment on O&M posts at those sites as well as the main site. Which raises the interesting issue, is the blog format obsolete? We started O&M in 2006, an eon ago in Internet time. Since then, Twitter, Facebook, Google Plus, LinkedIn, and other social media platforms have appeared, and they duplicate most functions of the old-fashioned blog. They usually allow cross-posting and let you compose on one and push to the others. So, are blogging platforms like WordPress (which we use) on the way out? Google’s unfortunate decision to kill Google Reader has some people suggesting that RSS itself is dead. What should we do, to stay on the cutting edge? What’s the future of structured online group discussion? Should we create the first MOOOB (Massively Open Online Organizations Blog)?

Coasean Bargaining Opportunity

| Peter Klein |

Forget Wrigley Field: here’s a colorful example for classroom discussions of property rights, external costs, bargaining, and the Coase Theorem. Literally colorful. (Via Bob Subrick.)

Incomplete Contracts and the Internal Organization of Firms

| Peter Klein |

That’s the title of a new NBER paper by Philippe Aghion, Nicholas Bloom, and John Van Reenen, indicating that organization design, from the perspective of incomplete-contracting theory, continues to be a hot topic among the top economists. Like all NBER papers this one is gated, but intrepid readers may be able to locate a freebie.

Incomplete Contracts and the Internal Organization of Firms

Philippe Aghion, Nicholas Bloom, John Van ReenenNBER Working Paper No. 18842, February 2013

We survey the theoretical and empirical literature on decentralization within firms. We first discuss how the concept of incomplete contracts shapes our views about the organization of decision-making within firms. We then overview the empirical evidence on the determinants of decentralization and on the effects of decentralization on firm performance. A number of factors highlighted in the theory are shown to be important in accounting for delegation, such as heterogeneity and congruence of preferences as proxied by trust. Empirically, competition, human capital and IT also appear to foster decentralization. There are substantial gaps between theoretical and empirical work and we suggest avenues for future research in bridging this gap.

I, Coke Can

| Peter Klein |

| Peter Klein |

Via Craig Newmark, a modern riff on Leonard Read’s classic:

The number of individuals who know how to make a can of Coke is zero. The number of individual nations that could produce a can of Coke is zero. This famously American product is not American at all. Invention and creation is something we are all in together. Modern tool chains are so long and complex that they bind us into one people and one planet. They are not only chains of tools, they are also chains of minds: local and foreign, ancient and modern, living and dead — the result of disparate invention and intelligence distributed over time and space. Coca-Cola did not teach the world to sing, no matter what its commercials suggest, yet every can of Coke contains humanity’s choir.

No surprises here to students of open innovation, but a vivid illustration nonetheless.

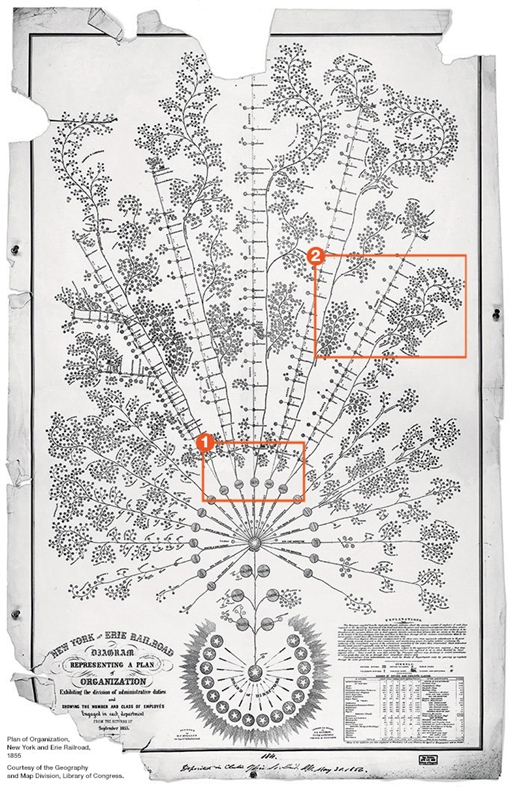

The First Modern Organizational Chart

| Peter Klein |

It was designed in 1854 for the New York and Erie Railroad and reflects a highly decentralized structure, with operational decisions concentrated at the local level. McKinsey’s Caitlin Rosenthal describes it as an early attempt to grapple with “big data,” one of today’s favored buzzwords. See her article, “Big Data in the Age of the Telegraph,” for a fascinating discussion. And remember, there’s little new under the sun (1, 2, 3).

Sequestration and the Death of Mainstream Journalism

| Peter Klein |

Much virtual ink has been spilled over the decline of the mainstream media, measured by circulation, advertising revenue, or a general sense of irrelevance. Usual explanations relate to the changing economics of news gathering and publication, the growth of social media, demographic and cultural shifts, and the like. These are all important but the main issue, I believe, is the characteristics of the product itself. Specifically, news consumers increasingly recognize that the mainstream media outlets are basically public relations services for government agencies, large companies, and other influential organizations. Journalists do very little actual journalism — independent investigation, analysis, reporting. They are told what stories are “important” and, for each story, there is an official Narrative, explaining the key issues and acceptable opinions on these issues. Journalists’ primary sources are off-the-record, anonymous briefings by government officials or other insiders, who provide the Narrative. A news outlet that deviates from the Narrative by doing its own investigation or offering its own interpretation risks being cut off from the flow of anonymous briefings (and, potentially, excluded from the White House Press Corps and similar groups), which means a loss of prestige and a lower status. Basically, the mainstream news outlets offer their readers a neatly packaged summary of the politically correct positions on various issues. In exchange for sticking to the Narrative, they get access to official sources. Give up one, you lose the other. Readers are beginning to recognize this, and they don’t want to pay.

Nowhere is this situation more apparent than the mainstream reporting on budget sequestration. The Narrative is that sequestration imposes large and dangerous cuts — $85 billion, a Really Big Number! — to essential government services, and that the public reaction should be outrage at the President and Congress (mostly Congressional Republicans) for failing to “cut a deal.” You can picture the reporters and editors grabbing their thesauruses to find the right words to describe the cuts — “sweeping,” “drastic,” “draconian,” “devastating.” In virtually none of these stories will you find any basic facts about the budget, which are easily found on the CBO’s website, e.g.:

- Sequestration reduces the rate of increase in federal spending. It does not cut a penny of actual (nominal) spending.

- The CBO’s estimate of the reduction in increased spending between 2012 and 2013 is $43 billion, not $85 billion.

- Total federal spending in 2012 was $3.53 trillion. The President’s budget request for 2013 was $3.59 trillion, an increase of $68 billion (about 2%). Under sequestration, total federal spending in 2013 will be $3.55 trillion, an increase of only $25 billion (a little less than 1%).

- Did you catch that? Under sequestration, total federal spending goes up, just by less than it would have gone up without sequestration. This is what the Narrative calls a “cut” in spending! It’s as if you asked your boss for a 10% raise, and got only a 5% raise, then told your friends you got a 5% pay cut.

- Of course, these are nominal figures. In real terms, expenditures could go down, depending on the rate of inflation. Even so, the cuts would be tiny — 1 or 2%.

- The news media also talk a lot about “debt reduction,” but what they mean is a reduction in the rate at which the debt increases. Even with sequestration, there is a projected budget deficit — the government will spend more than it takes in — during every year until 2023, the last year of the CBO estimates. The Narrative grudgingly admits that sequestration might be necessary to reduce the national debt, but sequestration doesn’t even do that. It’s as if you went on a “dramatic” weight-loss plan by gaining 5 pounds every year instead of 10.

This is all public information, easily accessible from the usual places. But mainstream news reporters can’t be bothered to look is up, and don’t feel any need to, because they have the Narrative, which tells them what to say. Seriously, have you read anything in the New York Times, Washington Post, or Wall Street Journal or heard anything on CNN or MSNBC clarifying that the “cuts” are reductions in the rate of increase? Even Wikipedia, much maligned by the establishment media, gets it right: ” sequestration refers to across the board reductions to the planned increases in federal spending that began on March 1, 2013.” If we have Wikipedia, why on earth would we pay for expensive government PR firms?

NB: See also earlier comments on the mainstream media here and here.

Russian Summer School on Institutional Analysis

| Peter Klein |

The Center for Institutional Studies at Russia’s Higher School of Economics sponsors an annual summer school “aimed at creating and supporting the academic network of young researchers from all regions of Russia as well as from CIS and other countries, who work in the field of New Institutional Economics.” This year’s conference is 29 June – 5 July in Moscow, and the faculty includes former O&M guest blogger Scott Masten along with John Nye, Russell Pittman, Garrett Jones, and many others. The full program, along with registration and other info, is available at the conference site.

My Response to Shane (2012)

| Peter Klein |

Peter Lewin blogged earlier on the ten-year retrospectives by Scott Shane and Venkataraman et al. on the influential 2000 Shane and Venkataraman paper, “The Promise of Entrepreneurship as a Field of Research.” As Peter mentioned, Shane acknowledges critics of the opportunity construct such as Sharon Alvarez, Jay Barney, Per Davidsson, and me, but dismisses our concerns as trivial or irrelevant.

The January 2013 issue of AMR includes a formal response by Alvarez and Barney, as well as rejoinders by Shane (with Jon Eckhardt) and Venkataraman (with Saras Sarasvathy, Nick Dew, and William Forster). The dialogue is well worth reading. I didn’t participate in the symposium but do have a brief response to Shane.

My critique of Shane’s work, and the opportunity-discovery perspective more generally, is that the scientific understanding of entrepreneurship has been held back by the focus on opportunities. The basic idea is simple: “opportunities” do not exist objectively, but are only only subjective images, or conjectures, about future possibilities. They exist in the mind of the entrepreneur, who takes actions to try to bring them about. The very concept of opportunity makes sense only ex post, after actions have been taken and future outcomes realized, leading to realized profits and losses. Under uncertainty, there are no opportunities, only entrepreneurial forecasts, which may turn out to be correct or incorrect. (My critique is slightly different from that of Alvarez and Barney, who argue that some opportunities are “discovered,” but others are “created.” My position is that the whole idea of opportunity is at best redundant, and at worst misleading and harmful.) I maintain that the unit of analysis in entrepreneurship research should be action (investment) under uncertainty, not the discovery (or creation) of profit opportunities.

These arguments are laid out in my 2008 SEJ article and in the Foss-Klein 2012 book. They also came to the fore in a recent exchange with Israel Kirzner, the intellectual father of the opportunity construct. (more…)

Doug Allen on Alchian

| Peter Klein |

A remembrance from our friend Doug Allen:

I only met Armen once, but his influence on me was profound. In the fall of 1980 I was taking intermediate micro economics to fulfill a Business Degree requirement. The course was taught by the great Art DeVany, who had been a student of Armen’s at UCLA. Naturally he used “Exchange and Production” as his text. I remember vividly the day — it was a Thursday, late on a cloudy afternoon — when I entered a corner of a large hallway on campus. I was thinking about the concept covered in class that week: “prices are not determined by costs.” I went into that corner thinking like an accountant, and when I came out the other side I was thinking like an economist. It was an epiphany. I came out thinking “of course prices are not determined by costs!”

I quickly changed majors, decided to postpone law school for a detour in graduate economics, and have never looked back. Fortunately for me my advanced undergraduate theory class was taught by Chris Hall, an intellectual grandson of Armen’s via Steve Cheung. His text for the course was “Economic Forces at Work.” I loved Armen’s writing, his style, and his ease in making life a big puzzle to solve.

I mentioned that I have only met the great man once. It was at a PERC conference in the early 1990s. The small group sat around tables in alphabetical order, and so Alchian was first and (Doug) Allen was second. I jokingly said “ah, Alchain and Allen, together again.” I thought it was quite witty, but Armen ignored the remark. I made some other comments that he was similarly impressed with. So, remembering that “even a fool is counted wise when he keeps his mouth shut,” I just sat back and listened. It was a great treat, and Armen didn’t seem to mind having me tag along for the weekend. My favorite recollection was a long discussion we had over how Rockefeller actually made money.

As I think about his passing, the one thought that strikes me is “where is the Armen Alchain for today?” Where is the economist’s economist? I suppose there just never will be another AAA.

Armen Alchian (1914-2013)

| Peter Klein |

Armen Alchian passed away this morning at 98. We’ll have more to write soon, but note for now that Alchian is one of the most-often discussed scholars here at O&M. A father of the “UCLA” property-rights tradition and a pioneer in the theory of the firm, Alchian wrote on a dizzying variety of topics and was consistently insightful and original.

Alchian was very intellectually curious, always pushing in new directions and looking for new understandings, without much concern for his reputation or legacy. One personal story: I once asked him, as a naive and somewhat cocky junior scholar, how he reconciled the team-production theory of the firm in Alchian and Demsetz (1972) with the holdup theory in Klein, Crawford, and Alchian (1978). Aren’t these inconsistent? He replied — politely masking the irritation he must have felt — “Well, Harold came to me with this interesting problem to solve, and we worked up an explanation, and then, a few years later, Ben was working on a different problem, and we started talking about it….” In other words, he wasn’t thinking of developing and branding an “Alchian Theory of the Firm.” He was just trying to do interesting work.

Updates: Comments, remembrances, resources, links, etc.:

- Robert Higgs

- David Henderson (1, 2)

- Jerry O’Driscoll

- Alex Tabarrok

- Doug Allen

- Dan Benjamin

- A 1996 Alchian symposium (gated)

- Alchian and Woodward’s review of Williamson (1985): “The Firm Is Dead, Long Live the Firm”

Recent Comments